All Categories

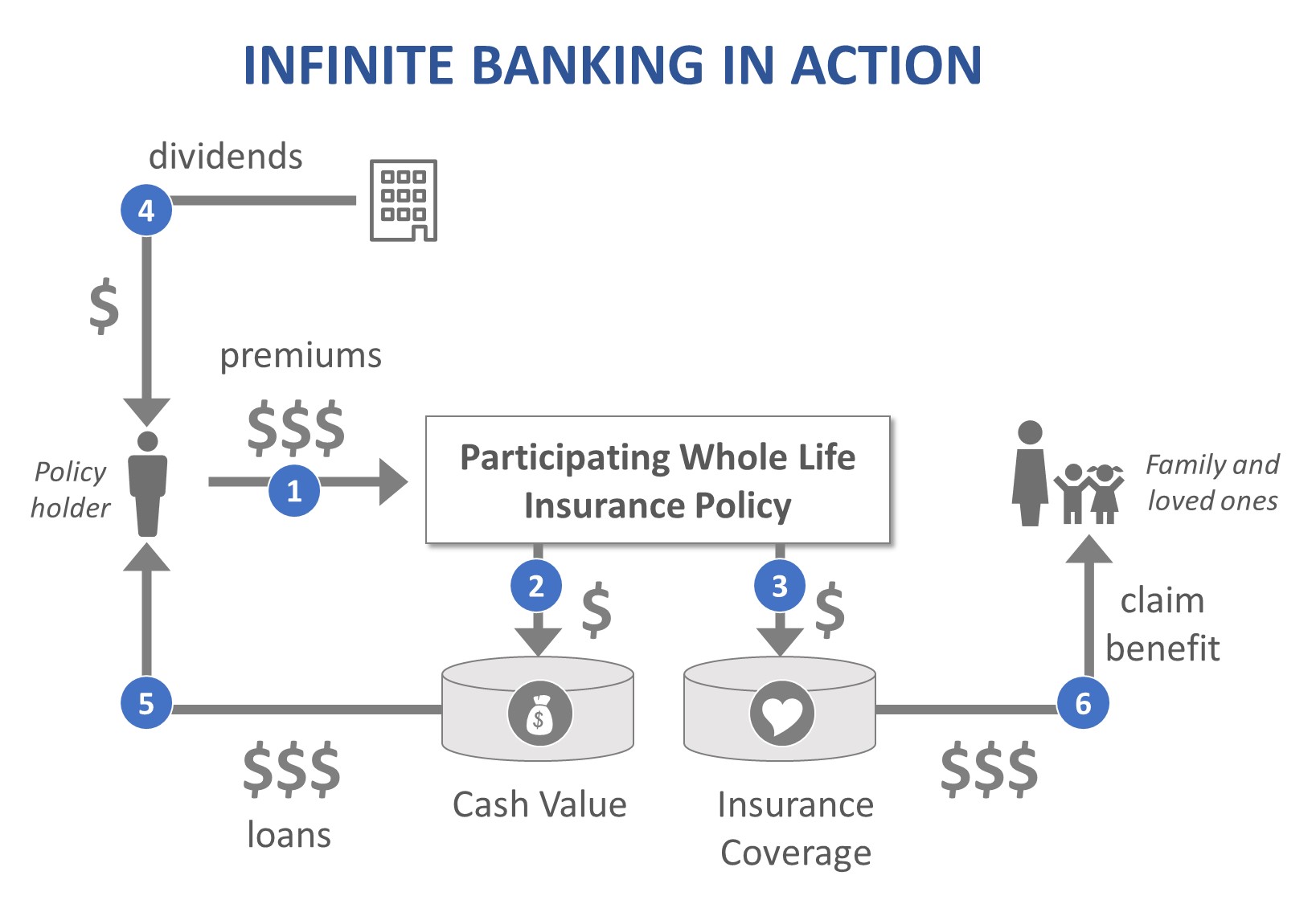

Featured

Table of Contents

The are entire life insurance policy and universal life insurance policy. The cash value is not added to the death advantage.

After one decade, the money worth has actually grown to roughly $150,000. He secures a tax-free lending of $50,000 to start a business with his bro. The policy lending rates of interest is 6%. He pays back the financing over the next 5 years. Going this course, the interest he pays goes back into his plan's cash money worth as opposed to a financial establishment.

Imagine never ever having to fret concerning financial institution fundings or high rate of interest prices once again. That's the power of limitless banking life insurance policy.

There's no set financing term, and you have the freedom to make a decision on the payment timetable, which can be as leisurely as repaying the finance at the time of death. This versatility includes the maintenance of the financings, where you can go with interest-only repayments, maintaining the car loan balance flat and convenient.

Holding money in an IUL dealt with account being credited interest can typically be far better than holding the money on deposit at a bank.: You've always fantasized of opening your very own bakeshop. You can borrow from your IUL plan to cover the first expenses of renting an area, acquiring equipment, and employing personnel.

Infinite Banking System Review

Personal car loans can be obtained from standard financial institutions and credit rating unions. Obtaining money on a credit report card is usually very expensive with annual percentage prices of passion (APR) often reaching 20% to 30% or even more a year.

The tax obligation treatment of plan financings can differ significantly depending on your country of home and the particular terms of your IUL plan. In some regions, such as The United States and Canada, the United Arab Emirates, and Saudi Arabia, policy lendings are generally tax-free, offering a substantial advantage. Nevertheless, in other jurisdictions, there may be tax ramifications to take into consideration, such as possible tax obligations on the financing.

Term life insurance policy only gives a fatality advantage, with no cash money value build-up. This indicates there's no cash value to borrow versus. This article is authored by Carlton Crabbe, President of Capital for Life, a professional in offering indexed global life insurance policy accounts. The details supplied in this post is for academic and informative objectives just and should not be interpreted as financial or investment guidance.

Direct Recognition Whole Life

When you initially become aware of the Infinite Banking Concept (IBC), your first reaction could be: This sounds as well good to be true. Perhaps you're skeptical and assume Infinite Banking is a fraud or scheme - how does bank on yourself work. We intend to set the record directly! The issue with the Infinite Financial Concept is not the concept yet those individuals providing a negative critique of Infinite Banking as a concept.

As IBC Authorized Practitioners via the Nelson Nash Institute, we believed we would certainly address some of the leading questions people search for online when finding out and comprehending everything to do with the Infinite Banking Idea. What is Infinite Financial? Infinite Financial was created by Nelson Nash in 2000 and completely clarified with the magazine of his publication Becoming Your Own Banker: Open the Infinite Banking Principle.

Own Your Own Bank

You think you are coming out economically in advance because you pay no rate of interest, yet you are not. With conserving and paying money, you might not pay rate of interest, but you are using your money once; when you invest it, it's gone for life, and you provide up on the possibility to earn life time substance passion on that money.

Billionaires such as Walt Disney, the Rockefeller family and Jim Pattison have leveraged the residential or commercial properties of entire life insurance policy that dates back 174 years. Even financial institutions use whole life insurance policy for the very same objectives. It is called Bank-Owned-Life-Insurance (BOLI). The Canada Profits Company (CRA) also acknowledges the worth of taking part whole life insurance policy as an unique property class utilized to create long-lasting equity securely and naturally and supply tax benefits outside the scope of traditional investments.

Standard Chartered Bank Visa Infinite Credit Card

It allows you to generate wide range by fulfilling the financial feature in your very own life and the ability to self-finance significant way of life purchases and expenses without interrupting the compound passion. One of the simplest means to think of an IBC-type participating entire life insurance policy policy is it approaches paying a mortgage on a home.

In time, this would create a "continuous compounding" impact. You get the picture! When you borrow from your participating entire life insurance policy, the cash money value proceeds to grow continuous as if you never ever obtained from it in the very first area. This is because you are making use of the money worth and fatality benefit as security for a financing from the life insurance policy company or as security from a third-party lender (referred to as collateral loaning).

That's why it's critical to deal with a Licensed Life Insurance coverage Broker authorized in Infinite Financial who structures your participating whole life insurance coverage plan appropriately so you can prevent negative tax obligation effects. Infinite Financial as a monetary approach is not for everyone. Below are a few of the benefits and drawbacks of Infinite Financial you ought to seriously consider in making a decision whether to move ahead.

Our preferred insurance policy carrier, Equitable Life of Canada, a mutual life insurance coverage firm, concentrates on taking part whole life insurance policy plans particular to Infinite Financial. Likewise, in a shared life insurance policy firm, insurance holders are thought about business co-owners and receive a share of the divisible excess created annually through dividends. We have an array of service providers to select from, such as Canada Life, Manulife and Sunlight Lifedepending on the demands of our customers.

Please likewise download our 5 Leading Concerns to Ask A Boundless Financial Agent Before You Work with Them. To learn more about Infinite Financial browse through: Please note: The product provided in this newsletter is for educational and/or academic functions just. The info, viewpoints and/or sights expressed in this e-newsletter are those of the authors and not always those of the representative.

Nelson Nash Ibc

The concept of Infinite Financial was developed by Nelson Nash in the 1980s. Nash was a money expert and follower of the Austrian school of business economics, which supports that the value of products aren't explicitly the outcome of typical economic structures like supply and demand. Instead, individuals value cash and products differently based upon their economic standing and requirements.

One of the mistakes of traditional banking, according to Nash, was high-interest prices on fundings. Too many people, himself included, got involved in financial difficulty due to reliance on banking institutions. So long as financial institutions established the rate of interest and lending terms, individuals really did not have control over their very own riches. Becoming your own lender, Nash determined, would place you in control over your financial future.

Infinite Banking needs you to own your monetary future. For goal-oriented people, it can be the best financial tool ever. Here are the advantages of Infinite Banking: Perhaps the single most advantageous facet of Infinite Banking is that it improves your cash money circulation.

Dividend-paying whole life insurance coverage is very low risk and uses you, the policyholder, a good deal of control. The control that Infinite Banking supplies can best be grouped into 2 categories: tax obligation benefits and possession securities. One of the factors whole life insurance policy is suitable for Infinite Banking is just how it's taxed.

Whole life insurance policy policies are non-correlated assets. This is why they function so well as the financial foundation of Infinite Banking. No matter what happens on the market (stock, genuine estate, or otherwise), your insurance plan preserves its worth. A lot of people are missing this important volatility buffer that assists secure and grow wide range, instead dividing their money into two pails: financial institution accounts and financial investments.

Whole life insurance policy is that third container. Not just is the rate of return on your whole life insurance plan assured, your fatality advantage and costs are also assured.

Infinite Banking Insurance Companies

Infinite Banking charms to those looking for better monetary control. Tax obligation efficiency: The money worth grows tax-deferred, and plan fundings are tax-free, making it a tax-efficient tool for constructing wide range.

Property protection: In lots of states, the cash money value of life insurance coverage is secured from creditors, including an extra layer of financial safety and security. While Infinite Financial has its values, it isn't a one-size-fits-all option, and it includes substantial drawbacks. Here's why it may not be the finest method: Infinite Financial often requires intricate plan structuring, which can confuse insurance policy holders.

{kind=link}

Latest Posts

Infinitebanking Org

How To Start Your Own Offshore Bank

Learn How To Become Your Own Bank!